Understanding SSAE 18: A Guide to Service Organization Control Reporting

SSAE 18

Sirr Gardener

4/13/20253 min read

In today's digitally driven world, businesses increasingly rely on third-party service providers for essential operations, from cloud hosting to payroll processing. This shift in operational dynamics brings a new set of risks, particularly around data security, financial integrity, and compliance. That’s where SSAE 18 comes into play—a framework designed to give assurance over the controls service organizations have in place.

In this blog post, we’ll break down what SSAE 18 is, why it matters, and how it affects organizations and auditors alike.

What is SSAE 18?

SSAE 18, short for Statement on Standards for Attestation Engagements No. 18, is an auditing standard issued by the American Institute of Certified Public Accountants (AICPA). It went into effect on May 1, 2017, replacing the older SSAE 16 standard.

SSAE 18 is primarily used to issue System and Organization Control (SOC) reports, which evaluate the internal controls of a service organization—an entity that provides outsourced services that impact the financial reporting or security posture of its clients.

The Purpose of SSAE 18

SSAE 18 was introduced to improve upon previous standards by:

Enhancing the clarity and consistency of attestation reports.

Requiring a better understanding of the service organization’s risk environment.

Tightening the requirements around monitoring subservice organizations (i.e., vendors of the service provider).

Emphasizing risk assessment procedures to evaluate the suitability of controls.

The standard applies not just to IT service providers, but also to companies in healthcare, financial services, logistics, and more.

SSAE 18 and SOC Reports

Under SSAE 18, auditors can issue three main types of SOC reports:

1. SOC 1

Focus: Internal controls over financial reporting (ICFR).

Audience: User auditors and controllers.

Relevance: Useful for clients whose financial reporting depends on the service organization’s systems (e.g., payroll processors).

2. SOC 2

Focus: Trust Services Criteria—Security, Availability, Processing Integrity, Confidentiality, and Privacy.

Audience: Business partners, regulators, and stakeholders concerned with operational risks and data security.

Relevance: Ideal for SaaS providers, data centers, and cloud services.

3. SOC 3

Focus: Same as SOC 2, but designed for general public consumption.

Audience: Broad, including potential customers.

Relevance: Used in marketing to demonstrate strong security controls.

Key Features of SSAE 18

Here are some of the most important aspects of SSAE 18:

🔎 Risk Assessment

Auditors must thoroughly understand the service organization’s environment and identify potential risks that could lead to material misstatements or control failures.

🔗 Vendor Management

Organizations must monitor subservice providers (e.g., cloud vendors or third-party data centers) and demonstrate that they have controls in place to manage associated risks.

📋 Management Assertions

Management of the service organization must provide a written assertion about the fairness of the presentation of the system and the suitability of the design and operating effectiveness of controls.

🧾 Complementary User Entity Controls (CUECs)

User organizations (i.e., clients) have responsibilities too. SSAE 18 includes CUECs—controls the user must implement for the service organization’s controls to be effective.

Benefits of SSAE 18 Compliance

Transparency: Builds trust with clients by showing an independent evaluation of your controls.

Risk Management: Highlights areas for improvement in internal control and third-party risk management.

Competitive Advantage: A clean SOC report under SSAE 18 enhances credibility in the marketplace.

Regulatory Alignment: Helps align with other frameworks like SOX, HIPAA, ISO 27001, and GDPR.

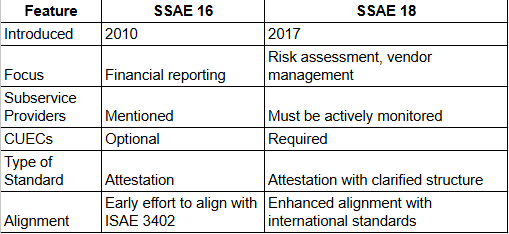

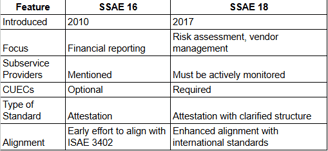

SSAE 18 vs. SSAE 16: What Changed?

Who Needs a SOC Report under SSAE 18?

Organizations that:

Handle sensitive data for clients.

Provide outsourced financial, IT, or operational services.

Are asked by customers for security or compliance assurance.

Want to stand out in competitive bids for contracts.

Final Thoughts

SSAE 18 is more than just an audit requirement—it’s a vital framework that demonstrates trust, security, and integrity in service delivery. Whether you're a service organization aiming to gain client confidence or a user organization trying to assess third-party risk, understanding SSAE 18 and its SOC reporting structure is essential.

As cyber threats and regulatory pressures increase, being proactive about SSAE 18 compliance can set your organization apart and position it for long-term success.

Further Reading

AICPA SOC Reports Overview: https://www.aicpa.org/soc

Trust Services Criteria (TSC) Explained

Differences Between SOC 1, SOC 2, and SOC 3 Reports